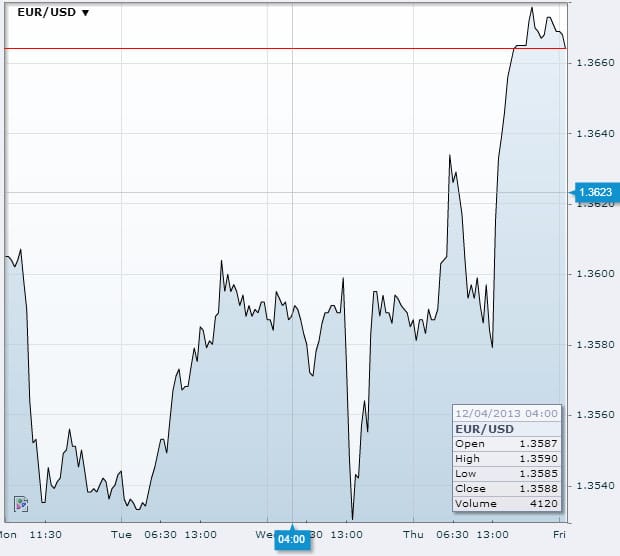

The euro rallied to a five-week high against the dollar in early trading in Asia this morning, after a pronouncement from ECB president Mario Draghi indicated that the bank is unlikely to introduce additional stimulus in the near future.

Although Draghi said the bank was ready to adapt its monetary policy if need be, his speech was light on details, with no mention of the potential use of a negative deposite rate.

Noting that liquidity in the banking system has improved since the last round of LTRO, Draghi said that any repeat of this operation would be conditional on a number of factors. On the back of these comments, German bond yields leapt to seven-week highs, adding further bullishness to the euro.

“The comments do not indicate any sense of urgency on the part of the ECB,” said Commonwealth Bank economist Martin McMahon, in a note to clients.

“If there is to be a new LTRO, the ECB wants ‘to make sure that it reaches the economy’. Again the comments do not indicate that follow-up LTROs are imminent.”

Source: fxstreet.com

At the time of writing, the euro was sitting at around the $1.3667 level, having climbed by more than 0.5% on Thursday to a five-week peak of $1.3677. It also moved up to 139.14 yen, but couldn’t break above the five-year peak of 140.03 set earlier this week.

Meanwhile, the Bank of England’s decision not to change interest rates saw the sterling fall to week-long-lows against the euro. The euro bought 83.68p, having been at 83.79 earlier in the day.

The euro rebound hit the dollar index, which reached a five-week low of 80.231. All eyes will be on the release of US jobs data this afternoon, which could tip the balance either way. A Reuters poll of analysts showed an average forecast of 180,000 created in November, a drop-off from the previous month’s 183,900.

A positive surprise could have the potential to accelerate the Fed’s plans to taper their bond-buying programme, perhaps from the date of their Dec 17/18 meeting – which would be a major booster for the greenback. However, if the figures come in as expected, or worse, then the expectation of continued monetary easing will be a downward push on the dollar, but will boost riskier assets such as equities.

Tradersdna is a leading digital and social media platform for traders and investors. Tradersdna offers premiere resources for trading and investing education, digital resources for personal finance, market analysis and free trading guides. More about TradersDNA Features: What Does It Take to Become an Aggressive Trader? | Everything You Need to Know About White Label Trading Software | Advantages of Automated Forex Trading