Over the past six months in Spain, there have been many vehement claims of an emergent economic recovery in these parts, usually proclaimed with Olympian authority. But does the data really support such exclamations?

One observes the headline seasonally adjusted unemployment rate published by Eurostat peaking in April this year at 26.5% of the labour force before falling down slightly during the summer. This, coupled with resurgent export growth and a positive GDP growth reading of 0.1% in the third quarter, has led many to declare the emergence of a recovery. But is this really so?

Looking at the labour market, it is clear from the recent quarterly survey conducted by INE that many people are simply giving up searching for work at all, or worse still, leaving the country entirely. This has the effect of artificially reducing the headline rate of unemployment masking the true picture.

One notes the rate of those becoming inactive in the labour market accelerating to 1.6% YoY in the third quarter. INE’s survey also shows that the Spanish working age population fell 33,000 in the third quarter of 2013 and by 370,000 compared to the same quarter of 2012. Such figures re-in force the ‘hysteresis’ hypothesis, namely that Spain’s growth rate will never return to its pre-crisis level as those long term unemployed become detached from the labour market and emigrants never return. For the record, the long term unemployment rate (% of unemployed out of work for over 1 year) now stands at 58.4%.

Metrics of employment as a leading indicator of a potential jobs market recovery have recently pointed to some stabilisation in contraction. However, over the past year, much of this effect has been a rebalancing from full time to part time employment and from permanent to temporary contracts.

This is borne out by the above chart (via @WEAYL) as hours worked in the economy continue to make new quarterly lows. This casts doubts over the quality of any stabilisation or small recovery that may or may not be developing.

Moving on to the wider macro economy, many are citing Spain’s rising exports as a clear sign of recovery as they have posted a 6.6% YoY gain for the first eight months of 2013. That said, the recent strength of the Euro could pose a problem, particularly given estimates that point to an export price elasticity that exceeds 1. However, thus far, the external balance has improved albeit through crushing imports and the domestic economy in general. Note that domestic demand fell 12.7% between 2007 and 2012. And so far in 2013 until August, industrial production is down 3.2% year to date.

It is unclear how long the so called positive sentiment being whipped up in the markets and from politicians will last. A key part of whether the dominant service sector of the economy is able to recover will be the consumer’s propensity to spend. But unfortunately the consumer is still highly indebted which, coupled with crippling high unemployment and a growing credit crunch, means any rebound is unlikely at best.

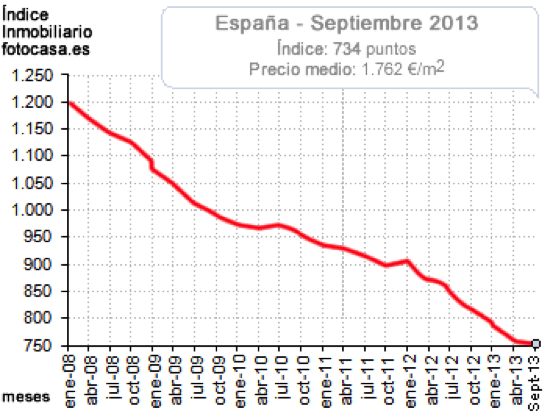

Source: fotocasa.es

The near 40pc drop in average home prices since the beginning of 2008 is only likely to continue as some estimates of unsold properties and those under construction still exceed 1.3 million. Spain’s bad bank also recently failed in its attempt to sell various real estate units with investors failing to offer bids deemed commercially acceptable. S&P reckons prices will not stop declining until 2016 at the earliest.

With the property bubble still deflating it is hard to see the domestic economy recovering (home ownership rates exceed 80%) enough to deliver economic fruits of jobs gains and wage growth. Further cuts to public budgets may now be looming since the EU on Tuesday revised Spain’s deficit forecast to 6.6% of GDP in 2015, well above the desired level. Should this materialise, and given the data this week confirming the onset of outright deflation, some say Spain could enter the classic liquidity trap. Under this scenario, containing the real value of the public debt amid falling prices in a credit starved, low growth economy would be enough to jolt the economy into a fresh downward spiral. With monetary policy remaining accommodative but proving ineffective, Spain could well be entering a sustained lost period of economic progress – hardly a recovery.

Tradersdna is a leading digital and social media platform for traders and investors. Tradersdna offers premiere resources for trading and investing education, digital resources for personal finance, market analysis and free trading guides. More about TradersDNA Features: What Does It Take to Become an Aggressive Trader? | Everything You Need to Know About White Label Trading Software | Advantages of Automated Forex Trading