Even though China has been stealing the show with the resurgence in volatility since the yearly reopening, the other major product that has been experiencing intraday swings of multiple percentage points has been crude oil. Even though recent inventory figures should have given oil a slight upside catalyst based on the massive drawdown in inventories, continued strong production figures and anticipation of a growing glut continue to weigh on prices of major benchmarks which have just fallen to new multi-year lows. The confluence of factors from rising production to weak demand will continue to weigh on prices until the imbalance corrects with itself and marginal producers are forced to quit producing due to lack of profitability.

Tale of Two Inventories

Traders might be quick to point out that the massive 5.085 million barrel drawdown in crude oil inventories should have been enough to send the West Texas Intermediate benchmark surging higher. However, a look behind the headline inventory number underlines that this reflects a refining gimmick versus an actual slowdown in production and uptick and demand. A look at distillate stockpiles alongside gasoline inventories shows the pace of refining likely accelerating, leading to surplus conditions and meaning weak end-user demand. Gasoline stockpiles rose at the fastest pace on record, climbing 10.576 million barrels last week, marking a 4.78% increase. Distillates rose by 4.12% over the same period in an indication that the equilibrium level for supply and demand remains elusive

While the drawdown in crude oil inventories saw an uptick in other areas of energy inventory, the real story is ever-rising inventories at the Cushing storage facility combined with rising production. Production last week rose by 20,000 barrels per day, with Cushing inventories gaining an additional 0.917 million barrels over the latest reporting period, marking 9-straight weeks of gains for the facility. Should gains continue apace, there is a possibility that inventories will be completely filled within a few short months, with onshore facilities across the globe feeling the same constraints. Although investors could cite current price momentum as evidence of the troubling times ahead for the energy industry, until producers are left with no other storage options and forced to dump production on the open market, further price declines will probably be moderated.

Below Breakeven

Some exploration and production companies will be forced to continue producing below break-even levels in order to go ahead and maintain land leases that allow for extraction. However, these sites are mostly smaller well owners with larger companies facing increasingly difficult conditions as banks decrease the amount of available credit, especially to shale producers. This is forcing companies to become more efficient in their production standards by trimming all available expenses down to the bone in an effort to stave off cash flow problems and possible bankruptcy.

The price war initiated by the Saudi’s looks unlikely to let up in 2016, especially now that other major producers have followed suit with Russia’s production overtaking the Gulf giant. While Middle East producers and Russia have the ability to extract crude oil at near rock-bottom rates, the goal of killing off North American unconventional oil plays has proven challenging. Production is actually higher than a year ago in the United States, and although risks are to the downside for the output going forward as producers try and exploit all possible efficiencies just to stay in business.

Chinese Demand Forecast to Rise

China’s insatiable demand for commodities has taken a big hit over the last year and crude oil finds itself in a similar quagmire. While consumption grew at a 1.50% annualized pace according to figures released back in November, mounting concerns about the domestic economy, particularly the manufacturing and industrial sectors could weigh on the outlook. Although forecasts currently expect Chinese imports of foreign oil to rise by approximately 8.00% in 2016, representing an additional 1 million barrels per day. This reflects the nation’s growing desire to raise domestic strategic petroleum reserve levels in an effort to protect against any emergency conditions. Additionally, aside from growing onshore storage, refiners are forced to keep production high in order to keep their government issued licenses for production

While this growth in demand may be enough to soak up rising exports expected to be unleashed by Iran in the coming months, other countries are seeing demand stagnate and even fall. Japan continues to see imports drop as the combination of greater energy efficiency and weak population demographics see a downshift in buying. This in many ways reflects conditions across many advanced economies as they try and reduce dependency on fossil fuels over time despite the relative benefit of buying energy at current price levels.

Fundamentally Speaking

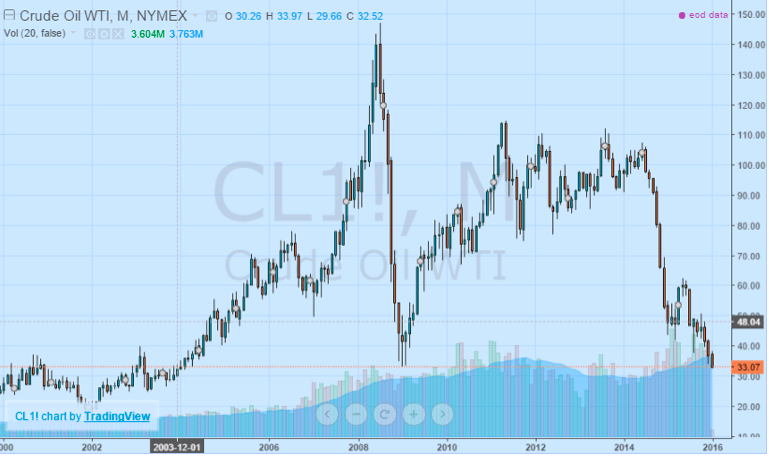

Current estimates point to the crude oil market being oversupplied to the tune of 1.500 to 2.000 million barrels per day. While rising demand from China might be able to offset some of the projected increases in production from Iran, prevailing conditions are unlikely to change until the supply-side of the equation is fixed by falling production from major global producers. Russia and Saudi Arabia in particular have prominently displayed their resistance to lowering production levels and in spite of weak prices, American production remains surprising robust While the drill rig count will probably fall further in coming months, it does not necessarily spell an end to falling prices.

With Brent and WTI both hitting multi-year lows during the overnight, a short-term bounce might be possible to the tune of several percent, but the long-term trends are likely to prevail, with any price rally an indication of an opportunity to initiate Put positions. Positions should largely target the next major psychological level of $30 per barrel with any break lower paving the way towards the low-to-mid $20s. While there may be a brief dead cat bounce in prices, momentum remains biased to the downside amid the myriad of factors contributing to oil’s demise. Until the supply and demand imbalance abates, the bearish tendencies of energy prices will remain unchanged over the medium-term.

Tradersdna is a leading digital and social media platform for traders and investors. Tradersdna offers premiere resources for trading and investing education, digital resources for personal finance, market analysis and free trading guides. More about TradersDNA Features: What Does It Take to Become an Aggressive Trader? | Everything You Need to Know About White Label Trading Software | Advantages of Automated Forex Trading