In the previous lesson, we explained what currency correlations are, and why they are useful for forex traders. Today, we’re going to show you how to interpret a currency correlation table, and also how to calculate correlations on your own.

Reading Currency Correlation Tables

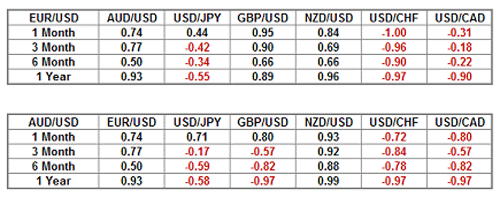

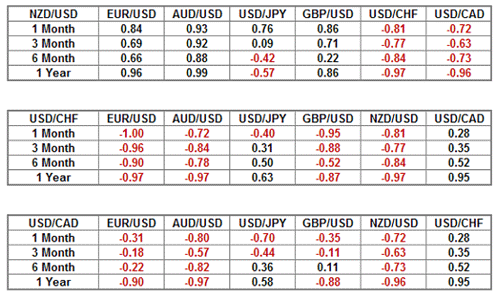

A currency correlation table usually takes the form of having the main currency pair in the top left corner, above a column of different time frames, and the pairs that it will be compared to along the top. The rest of the table gives the corresponding coefficient for each of these time frames. Let’s take a look at two tables from the month of February 2010 to illustrate:

Source: Investopedia

The top table shows correlations between EUR/USD and the other major currency pairs. As we can see, during February (1 month), EUR/USD and GBP/USD had a coefficient of 0.95 – a very strong positive correlation. What this means is that when EUR/USD rose, 95% of the time GBP/USD rose in tandem with it. The correlation wasn’t so strong over a six month time frame (0.66) but over the course of a year the pairs still show a strong correlation (0.89).

From the table, we can also see that the EUR/USD and USD/CHF had a perfect negative correlation of -1.00. This means that in 100% of cases during February, USD/CHF fell when EUR/USD rose. While the longer time frames show a slightly less perfect correlation, it still indicates a certain stability in that they are all quite similar.

Source: Investopedia

As we mentioned in the previous lesson, correlations do not always remain stable. For example, USD/CAD and USD/CHF had a strong positive correlation over the past year, but during February, this figure fell dramatically – in this case due to a surge in oli prices and a hawkish approach to monetary policy by Canada’s central bank.

Calculating Correlations

One way to ensure that the correlations you are referring to are accurate and up to date is to calculate them yourself using a spreadsheet such as Microsoft Excel. You’ll be pleased to hear that this isn’t as tricky as it sounds – especially when you realise that there is a function in Excel designed specifically for this.

Most charting packages will enable you to download historical daily currency prices in a format that can be imported into Excel. Once you have the data in your spreadsheet, all you need to do is use Excel’s =CORREL(range 1, range 2) command. Most people tend to use time frames of a year, six months, three months, and one month, but it is up to you to set these parameters as you see fit.

The first thing you need to do is to obtain the pricing data for your two pairs – for example EUR/USD and USD/CHF. Then, you need to create two columns for each of these pairs, filling the columns with the past daily prices for each pair during your specified time frame.

In an empty slot at the bottom of one of the columns, type in =CORREL( and highlight all the data in one of the columns – this should give you a range of cells in the formula box.

Now we need to type a comma, and select the data in the other column before closing the formula. It should now look something like this =CORREL(A1:A50,B1:B50) , and the number that is produced represents the correlation between the two pairs.

Despite the fact that correlations are almost always changing, you don’t have to update your numbers every day – every few weeks, or at the very least every month, should be sufficient.

In the third and final part of our series on currency correlation, we’ll be looking at the various ways in which you can use these to your advantage when trading.

Tradersdna is a leading digital and social media platform for traders and investors. Tradersdna offers premiere resources for trading and investing education, digital resources for personal finance, market analysis and free trading guides. More about TradersDNA Features: What Does It Take to Become an Aggressive Trader? | Everything You Need to Know About White Label Trading Software | Advantages of Automated Forex Trading