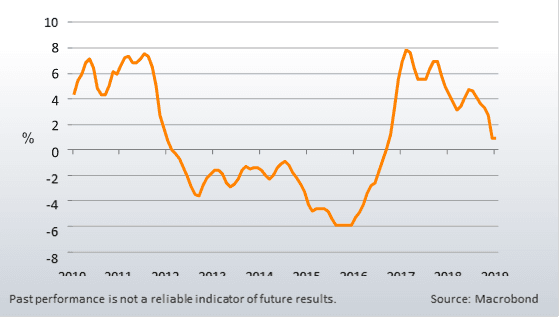

Chinese ‘factory gate’ price inflation has been slowing over the past two years. Recently released producer price inflation was markedly lower in year-on-year terms, driven down further by a very weak monthly reading in December. These lower ‘factory gate’ prices are likely to be imported into developed markets via trade with China, creating a disinflationary (slower inflation) impulse for developed economies. This would be good news for bond markets, which are notoriously unnerved by too much inflation.

It is important to note that disinflation is a term commonly used by the Federal Reserve to describe a period of slowing inflation. Unlike inflation and deflation, which refer to the direction of prices, disinflation refers to the rate of change in the rate of inflation. Although sometimes confused with deflation, disinflation is not considered as problematic because prices do not actually drop, and disinflation does not usually signal the onset of a slowing economy. Deflation is represented as a negative growth rate, such as -1%, while disinflation is shown as a change in the inflation rate from 3% one year to 2% the next.

“As such, the developed world has a potential counterbalance to these disinflationary pressures: strong domestic labour markets. US unemployment levels are currently at their lowest point since the 1970s, and even in Europe (where unemployment is structurally higher) employment levels are relatively robust,” said Graham Bishop, Investment Director at Heartwood Investment Management, the asset management arm of Handelsbanken in the UK.

In fact, as the US Federal Reserve has pointed out, the inflation remains on track for now, amidst signals of being slowed down, prior their next meeting. In it, it is due that policymakers discuss about the current rates of inflation and make efforts in tracking the control of the prices to reach their target of 2 per cent, as long as the American Jobs market and the unemployment rate keep steady at a 4 per cent rate.

“This in turn should feed through into wage inflation, which could work to offset the disinflationary impulses imported from China. While we expect these two factors to offset one another to a degree, we believe that for developed world economies the inflationary effects of strong labour markets at home will outweigh the disinflationary impulses from abroad, for now. As a result, we maintain our preference for short-duration fixed income assets, which are less likely to be impacted by changes in inflation,” concluded Graham Bishop.

Read More:

What is emotionless option trading?