More than 60% of financial institutions globally are now adopting AI in at least one business unit, reports Deloitte. From trading floors to customer service, automation and AI are now essential tools in modern finance. But are we ready for the ethical, regulatory, and workforce challenges this technology brings along?

When I first began exploring the intersection of finance and technology, it was clear to me that automation and AI were going to change everything. What used to be led by manual inputs, spreadsheets, and human guesswork is now being transformed by systems that learn, adapt, and operate at lightning speed.

According to McKinsey & Company, around 78% of organisations use AI in at least one business function, a sharp rise from 55% just two years earlier. In financial trading, AI now handles almost 89% of global trading volume, spanning high-frequency equity trades to decentralised crypto markets. The global algorithmic trading market is expected to continue growing, reaching around USD 38 billion by 2029.

But how did we go from spreadsheets and pens to AI trading millions in milliseconds?

This shift didn’t happen overnight.

But over the years, I’ve watched banks, investment firms, and fintech startups wake up to the realisation that old systems can no longer keep up. Markets move too fast.

Customers want personalised services around the clock. Regulations change constantly. Humans alone just can’t process this pace, and that’s where automation and AI step in.

But is this shift just about speed and cost, or are we entering a new era entirely?

Related Content: pre market trading

Automation’s journey in finance

Automation in finance started with basic tasks. In the early 1800s, Charles Babbage built the Difference Engine and Analytical Engine, early mechanical calculators that laid the groundwork for automating complex calculations. These machines influenced future digital computing and inspired key theoretical frameworks for programmable machines.

In the 20th century, John von Neumann’s computer architecture introduced the idea of a CPU that could store and execute instructions, key to real-time data processing and modelling in finance. His contributions underpinned the development of ENIAC and EDVAC, systems that facilitated large-scale financial simulations and statistical analysis.

A major milestone came in the 1980s when Thomas Peterffy introduced electronic trading, laying the foundation for algorithmic decision-making. By the 1990s, algorithmic trading became standard. These systems analyse data and execute trades faster than any human could. High-frequency trading today moves at milliseconds, and slow human decisions are no longer acceptable.

In recent years, robotic process automation (RPA) has gained traction in banks to handle repetitive operations, account onboarding, KYC checks, and regulatory filing. This allowed institutions like Deutsche Bank and HSBC to cut operational costs while improving speed and accuracy.

Automation has moved from back-office payroll to centre-stage trading systems. It is now deeply embedded in how finance works.

AI: The power behind modern finance

AI has moved beyond theory into action. Language models like LLMs (Large Language Models) and NLMs (Neural Language Models) can understand and generate language, powering advanced systems in customer service, fraud detection, and investment decisions.

Take JPMorgan’s COiN platform. It uses NLP (Natural Language Processing) to review millions of legal documents, saving thousands of hours of manual labour.

In investment, BlackRock’s Aladdin platform analyses risk and manages assets. Betterment uses AI to automate investment strategies, while Kavout predicts stock movements. These systems make sense of vast data streams, historical trends, social sentiment, and economic indicators faster than any human analyst.

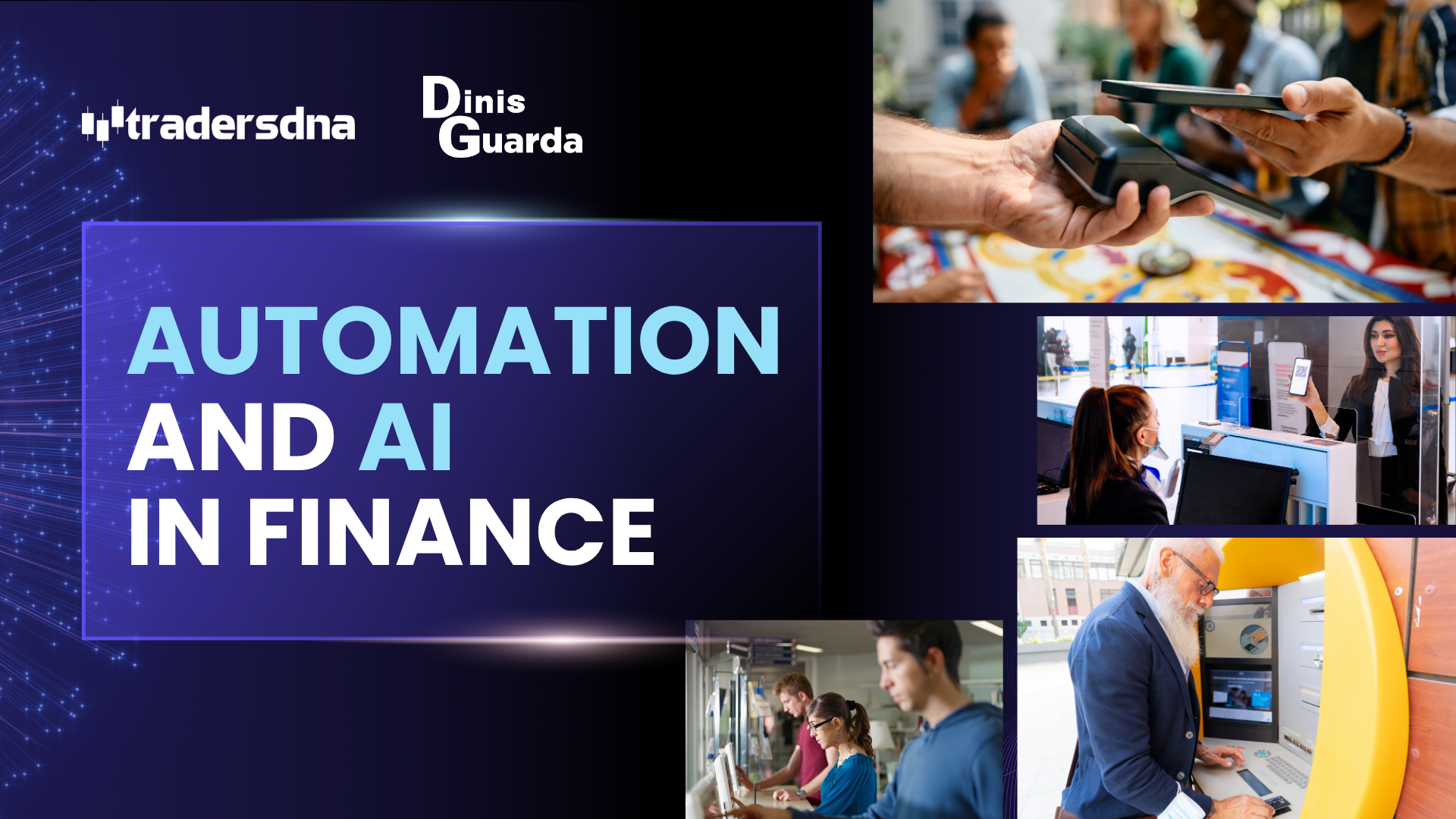

Hedge funds like Renaissance Technologies use AI-driven models to detect market patterns and execute trades without human input. These models don’t just react, they predict, allowing firms to stay one step ahead.

Other use cases include:

- Sentiment analysis from platforms like Accern and Dataminr to inform real-time market moves.

- Predictive modelling using deep learning to determine asset price volatility.

- AI-generated research reports reduce the need for human analysts.

AI in customer service and personalisation

Customers today want speed and personal attention. AI is making that possible.

Chatbots powered by NLP can now answer common queries and even offer tailored financial advice. Revolut uses a bot named Rita for customer support. It learns from each interaction, becoming more accurate over time.

American Express uses an AI assistant in its mobile app. It helps customers manage accounts and transactions, and it has improved customer satisfaction by 64%.

AI can also suggest savings plans or investments based on user behaviour, giving people financial tools that match their unique needs—without human involvement.

Bank of America’s virtual assistant, Erica, has surpassed 1.5 billion interactions since launch, providing proactive insights to users about their spending habits, alerts, and budgeting advice. These AI assistants also reduce customer service costs while increasing operational efficiency.

Managing risk and combating fraud

AI tools like Kensho and Ayasdi analyse massive datasets to spot irregularities or market shifts before they happen. In lending, AI systems go beyond traditional credit scores. Tools like Zest AI and LenddoEFL assess risk using alternative data—spending habits, online behaviour, and more.

This helps lenders include people who might be overlooked by traditional methods, but it also raises privacy concerns. With AI models relying on personal data, regulation is needed to prevent misuse.

Cybercrime is a constant threat. AI helps by monitoring transactions in real time. For example, Capital One uses Darktrace’s AI to detect anomalies. In 2019, it stopped an insider from leaking customer data thanks to this system. These tools learn over time and become better at stopping fraud while reducing false alerts.

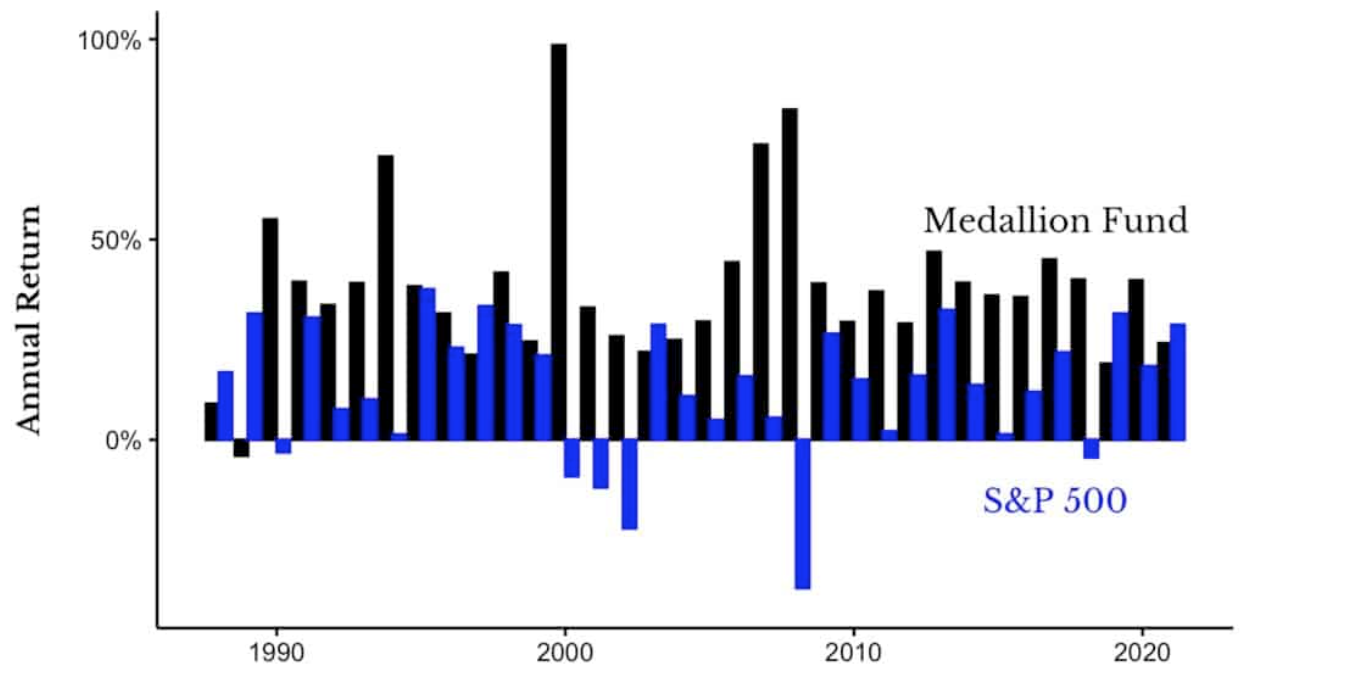

In 2023, Mastercard used AI to block over $30 billion in attempted fraud across payments, using an advanced behavioural analytics engine that monitors transaction velocity and geolocation mismatches.

The ethical dilemma: Bias and fairness in AI

AI models are only as fair as the data they’re trained on. If the data is biased, the outcomes will be too.

In 2019, Apple’s credit card, issued by Goldman Sachs, was criticised for giving women lower credit limits than men, even with similar financial profiles.

On a larger scale, the 2010 Flash Crash saw $1 trillion vanish from markets in minutes, triggered by AI trading systems reacting to each other. The problem wasn’t just speed—it was the lack of human oversight.

JP Morgan Chase was fined $920 million for spoofing trades using algorithms. These examples show how AI, if unchecked, can lead to market manipulation and unfair practices.

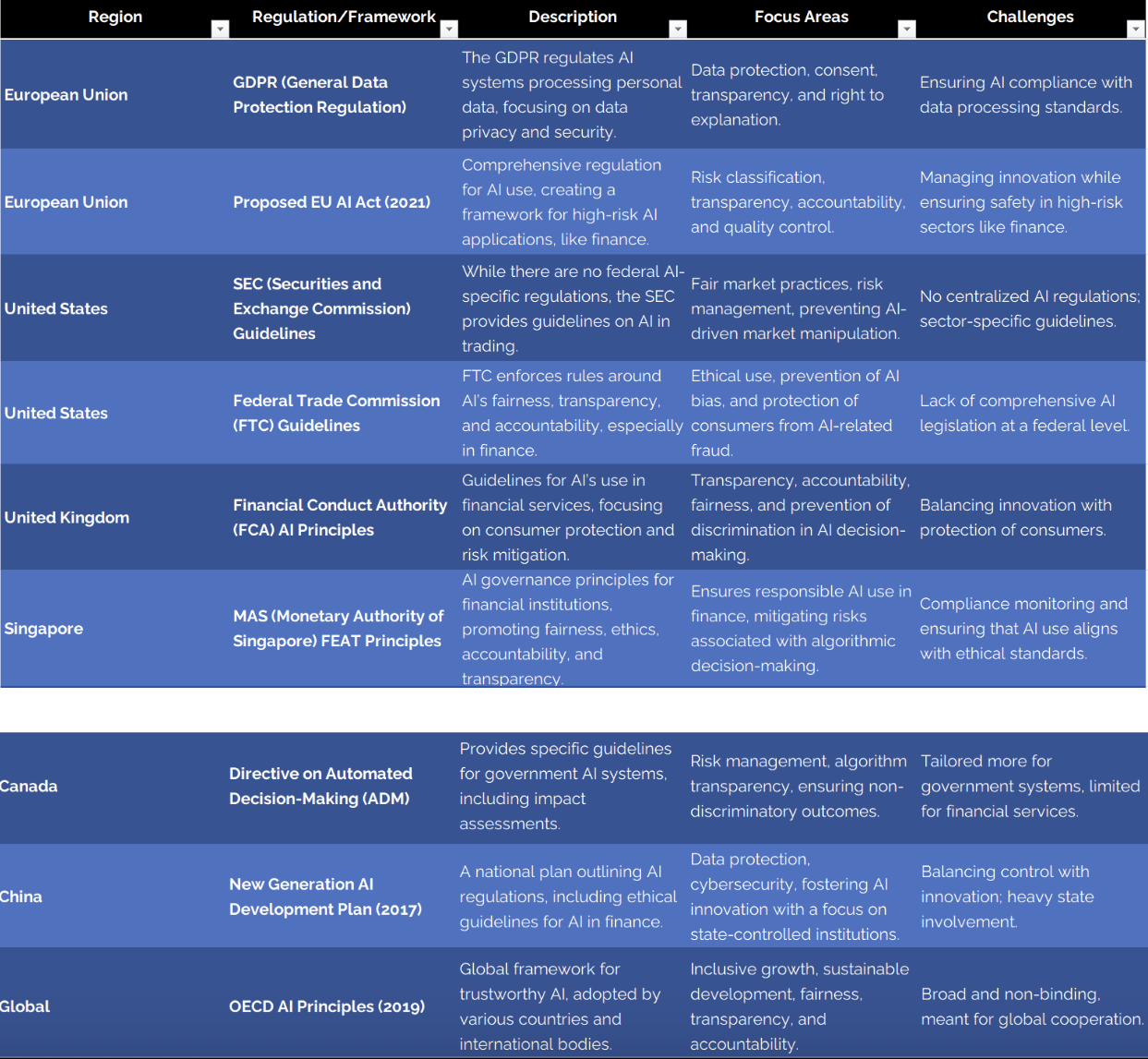

Bias also affects hiring, loan approvals, and insurance assessments. Organisations must conduct algorithmic audits and follow ethical AI frameworks to ensure fairness. The EU’s proposed AI Act will categorise use cases by risk and require rigorous transparency for high-risk applications.

Read More:

The workforce of the future

Automation is replacing many routine jobs—data entry, report writing, transaction handling. According to PwC, 30% of jobs are at risk of automation by the 2030s.

But new roles are emerging. Skills in AI governance, data science, and cybersecurity are in high demand. Workers who can interpret AI outputs and make strategic decisions are essential.

As Michael Figueroa of Toptal points out, companies are now hiring based on skills, not just roles. The future workforce will combine machine intelligence with human judgement.

Financial institutions are investing in reskilling programmes. Citi and JPMorgan have launched internal AI academies to train employees in machine learning, ethics, and data literacy. The workforce of tomorrow will be a hybrid of technical and strategic thinkers.

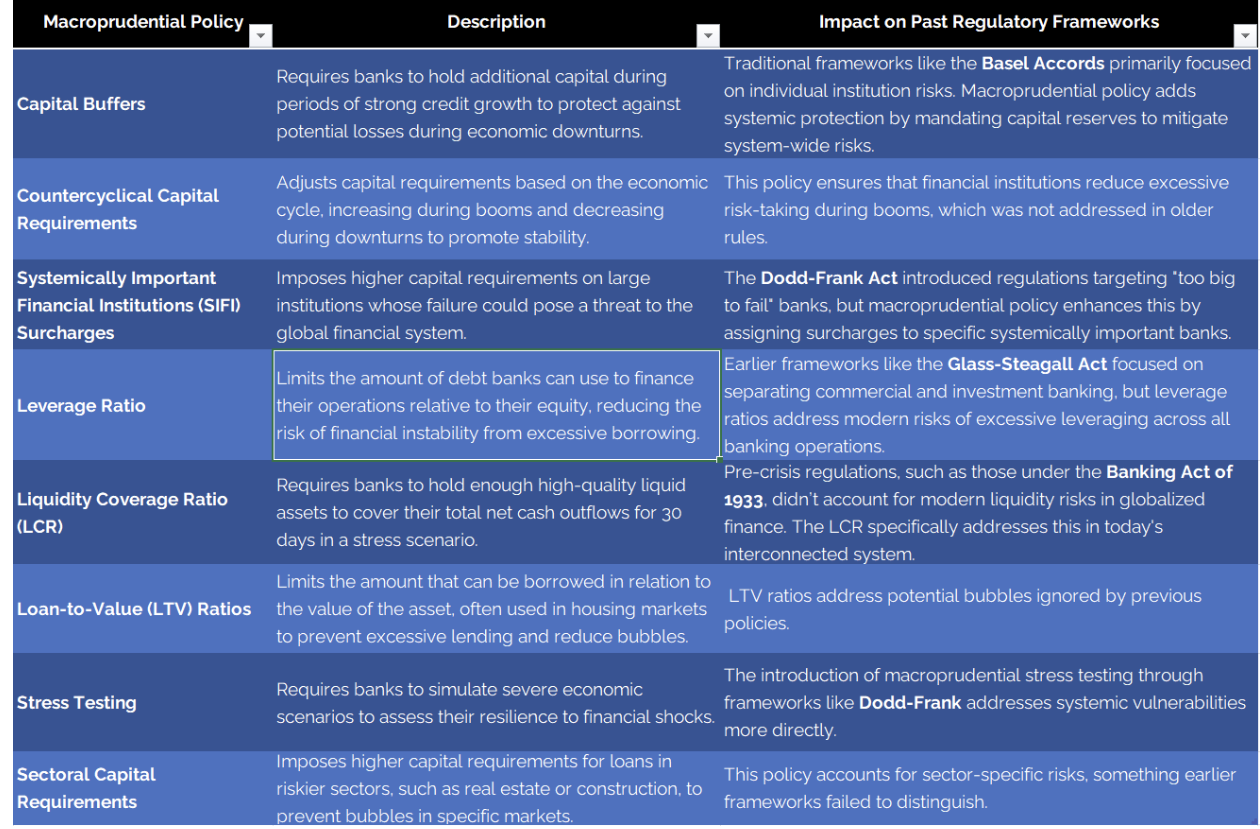

Regulatory challenges in an AI-driven world

Laws like the Securities Act and the Banking Act of 1933 were written before AI existed. They don’t account for algorithms that learn, change, and make decisions without human input.

This creates a gap. Regulators now require explainable AI systems where institutions can show how decisions were made, especially in areas like lending.

AI governance will become a major part of finance, ensuring that innovation does not come at the cost of privacy, fairness, or accountability.

The Financial Stability Board (FSB) and Bank of England are pushing for model transparency. Meanwhile, the EU’s Digital Operational Resilience Act (DORA) mandates financial entities ensure the resilience of their AI systems against cyber and operational risk.

Read More: sway markets

The convergence of AI and blockchain

AI and blockchain together are redefining trust, security, and automation in finance.

Platforms like Fetch.AI use AI agents to perform smart contracts, data sharing, and DeFi tasks. These systems are decentralised, meaning there is no single point of failure.

Dr Paolo Tasca highlights how decentralisation increases trust and security by distributing control.

AI offers real-time analysis, while blockchain ensures every action is transparent and traceable. Smart contracts allow complex financial transactions to run without intermediaries, cutting costs and delays.

Numerai, a hedge fund, uses AI models developed by a global community and stores transactions on blockchain via the Erasure protocol.

During COVID-19, AI helped banks adjust their risk strategies quickly. Blockchain ensured secure, transparent operations during this time.

Platforms like TradeLens (by IBM and Maersk) use blockchain for global logistics—cutting fraud and improving efficiency. These examples show the strength of combining AI intelligence with blockchain transparency.

A financially and ethically balanced future

Automation and AI are here to stay. They are transforming finance by increasing speed, improving decision-making, and opening up services to more people.

But with this power comes responsibility. The financial sector must ensure fairness, prevent bias, protect privacy, and follow clear ethical guidelines.

The future lies in balance—where AI enhances human work, and both operate within a strong ethical and regulatory framework.

Dinis Guarda is an author, academic, influencer, serial entrepreneur and leader in 4IR, AI, Fintech, digital transformation and Blockchain. With over two decades of experience in international business, C level positions and digital transformation, Dinis has worked with new tech, cryptocurrencies, drive ICOs, regulation, compliance, legal international processes, and has created a bank, and been involved in the inception of some of the top 100 digital currencies.

Dinis has created various companies such as Ztudium tech platform a digital and blockchain startup that created the software Blockimpact (sold to Glance Technologies Inc) and founder and publisher of intelligenthq.com, hedgethink.com, fashionabc.org and tradersdna.com. Dinis is also the co-founder of techabc and citiesabc, a digital transformation platform to empower, guide and index cities through 4IR based technologies like blockchain, AI, IoT, etc.

He has been working with the likes of UN / UNITAR, UNESCO, European Space Agency, Davos WEF, Philips, Saxo Bank, Mastercard, Barclays and governments all over the world.

He has been a guest lecturer at Copenhagen Business School, Group INSEEC/Monaco University, where he coordinates executive Masters and MBAs.

As an author, Dinis Guarda published the book 4IR: AI, Blockchain, FinTech, IoT, Reinventing a Nation in 2019. His upcoming book, titled 4IR Magna Carta Cities ABC: A tech AI blockchain 4IR Smart Cities Data Research Charter of Liberties for our humanity is due to be published in 2020.

He is ranked as one of the most influential people in Blockchain in the world by Right Relevance as well as being listed in Cointelegraph’s Top People In Blockchain and Rise Global’s The Artificial Intelligence Power 100. He was also listed as one of the 100 B2B Thought Leaders and Influencers to Follow in 2020 by Thinkers360.