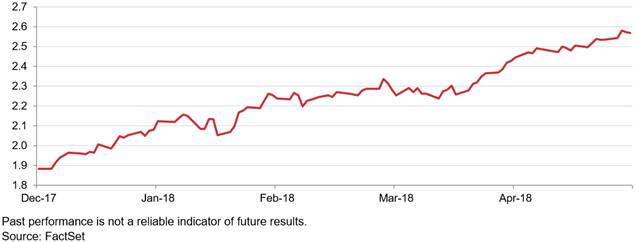

It has been a tough start to 2018 for bond investors, with government and corporate bonds across the globe delivering capital losses (yields rising). The US has led the way, with the short-medium section of the US yield curve moving up the most. This has been driven by fears of rising inflation and the prospect of interest rate increases beyond those previously forecast. This yield curve move has infected corporate bonds and emerging bonds, culminating in negative returns for both asset classes. Notably, though, credit spreads have barely moved this year, suggesting investors remain sanguine about default risk.

Bond yields have risen since the start of 2018

Yet valuations remain dear for sterling investors

One might, therefore, be expecting us to increase our bond exposure in order to take advantage of higher yields. However, we are not minded to do so for three reasons. First, we expect inflation to continue to pick up, potentially pushing yields higher still and deliver further capital losses to bond holders. Second, valuations still look unattractive in most areas of fixed income. Finally, whilst US treasury, corporate and EM dollar-denominated bonds are all yielding more than they were at the start of the year, the cost of hedging US dollar / sterling has rocketed this year, thereby reducing potential returns to sterling investors. We normally look to hedge our overseas bond holdings because otherwise currency movements tend to swamp the underlying bond return.

One niche market offering a glimmer of hope

Despite the bleak backdrop for fixed income investors, we have managed to identify one area of relative value; European Asset Backed Securities (ABS). These are bonds backed by consumer debt such as mortgages and credit cards. However, unlike their US counterparts, European ABS issuers are forced to retain 5% of each issue, thus aligning the interest of the issuer and investors, such as ourselves.

Perhaps due to stigma and complexity, these bonds offer superior yields when compared to traditional assets and additionally, pay floating rate coupons, thereby reducing interest rate risk. Pleasingly, our European ABS positions have managed to grind out small positive returns so far in 2018 – a tiny splash of green in an otherwise sea of red. Meanwhile, we are keeping our government and corporate bond exposure short-dated and high quality, patiently waiting for value to return to more traditional fixed income markets.

Read More:

how long after taking suboxone can you drive

what are ict concepts in trading?

how to avoid revenge trading forex factory?

Tradersdna is a leading digital and social media platform for traders and investors. Tradersdna offers premiere resources for trading and investing education, digital resources for personal finance, market analysis and free trading guides. More about TradersDNA Features: What Does It Take to Become an Aggressive Trader? | Everything You Need to Know About White Label Trading Software | Advantages of Automated Forex Trading