Overoptimism and overconfidence are two well-known psychological traits of our species. They are particularly dangerous in the late stages of an economic cycle where these terrible twins result in investors overestimating return and underestimating risk – a potentially lethal combination of errors.

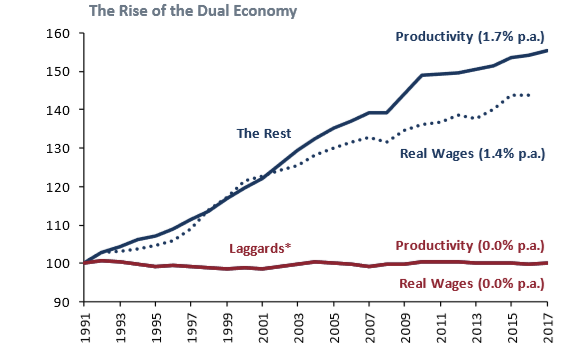

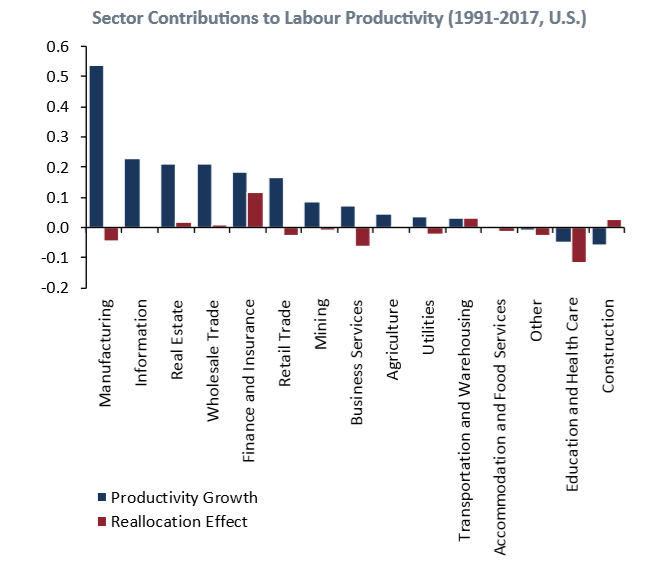

Far from the sanguine consensus of the current state of health of the U.S. economy, in this paper I demonstrate that this is the slowest and weakest recovery in post war history. Whilst GDP growth has been poor, labour productivity growth has been worse, and real wage growth worst of all. The headline data obscure even more worrying trends. Effectively, the U.S. is witnessing the rise of the “dual economy” – where productivity growth is reasonable in some sectors, and totally absent in others. Even in the sectors with good productivity growth, real wages are lagging (wage suppression is occurring). All the employment growth we are seeing is coming from the low productivity sectors. On top of this, the paltry gains in income that are being made are all going to the top 10%. This is not what a booming economy should feel like.

Real earnings growth in the corporate sector has been below the rate of GDP growth even after the significant boost from the financial engineering known as buybacks. So investors have little to celebrate. Indeed, a breathtaking 25% to 30% of firms in the Russell 3000 are actually loss-making! Yet the stock market remains well bid. In large part, this bid is sourced from the buybacks (and mergers) from USA Inc. itself. However, individual investors have returned to the “party” – never a good sign. Other portents of late-cycle capitulation include global fund managers throwing in the towel and buying into U.S. equities.

The corporate bid is really a massive debt for equity swap, with firms issuing massive amounts of corporate bonds (very low quality debt at that), and effectively leveraging themselves up. This creates a systemic vulnerability, and is potentially a Minsky Moment in the making. The listed sector has been at the vanguard (or perhaps better described as the forlorn hope) of this movement.

All of this occurs against a backdrop of an extremely expensive U.S. equity market, which is increasingly looking like Wile. E. Coyote – the hapless adversary of Roadrunner – having run off the edge of a cliff only to realise the ground is no longer below his feet. Tragically, it seems valuation is doomed to suffer Cassandra’s curse at a time when telling the truth is never believed.

In order to believe that U.S. equities are going to generate a “normal” return from these levels, you have to believe some quite extraordinary things. Perhaps you believe that P/Es are going to soar to levels not even seen at the height of the TMT bubble; or perhaps you believe that profitability is going to rise (from already extended levels) so that every firm in the U.S. looks like a FAANG stock; or perhaps you believe that growth is simply going to reach unprecedented levels. We, however, are not so prone to flights of fancy that require multi standard deviation outcomes. Unless you believe one of these extreme scenarios, you should be skeptical about the ability of the U.S. market to continue its outstanding performance. Ask yourself how much exposure you have to the U.S. stock market. Then ask yourself what is the minimum amount you could own. We at GMO own essentially zero in our unconstrained portfolios, but then again we are used to career risk and would rather run it than allocate to such an expensive and risky asset.

Article written by James Montier

Tradersdna is a leading digital and social media platform for traders and investors. Tradersdna offers premiere resources for trading and investing education, digital resources for personal finance, market analysis and free trading guides. More about TradersDNA Features: What Does It Take to Become an Aggressive Trader? | Everything You Need to Know About White Label Trading Software | Advantages of Automated Forex Trading