Online trading is booming, but so are payment risks. High-risk merchant accounts give traders secure processing, AI-driven fraud checks, and global reach despite higher costs. With chargeback thresholds around 1% flagged by Visa and Mastercard, how prepared are traders to manage risk and grow safely?

Trading has become more global than ever. The forex market processes over $7.5 trillion daily, while crypto trading volumes regularly cross $100 billion a day. More people are investing from their phones than ever before, making payments a critical part of every trade.

Why do banks see traders as risky clients?

Studies show that industries like forex, crypto, and online trading can face chargeback rates up to 1%–2%, much higher than the safe zone of 0.5%. When numbers cross that level, providers tighten rules or shut down accounts.

This is where High Risk Merchant Accounts step in.

They give traders the ability to process global payments, protect against fraud, and meet compliance standards.

The real question is: in a market moving this fast, are traders ready to handle the risks that come with growth?

What is a high risk merchant account?

A High Risk Merchant Account is a type of bank account designed for businesses that deal with industries or transactions considered risky by payment providers. Risk is usually linked to the chance of fraud, chargebacks, or legal restrictions.

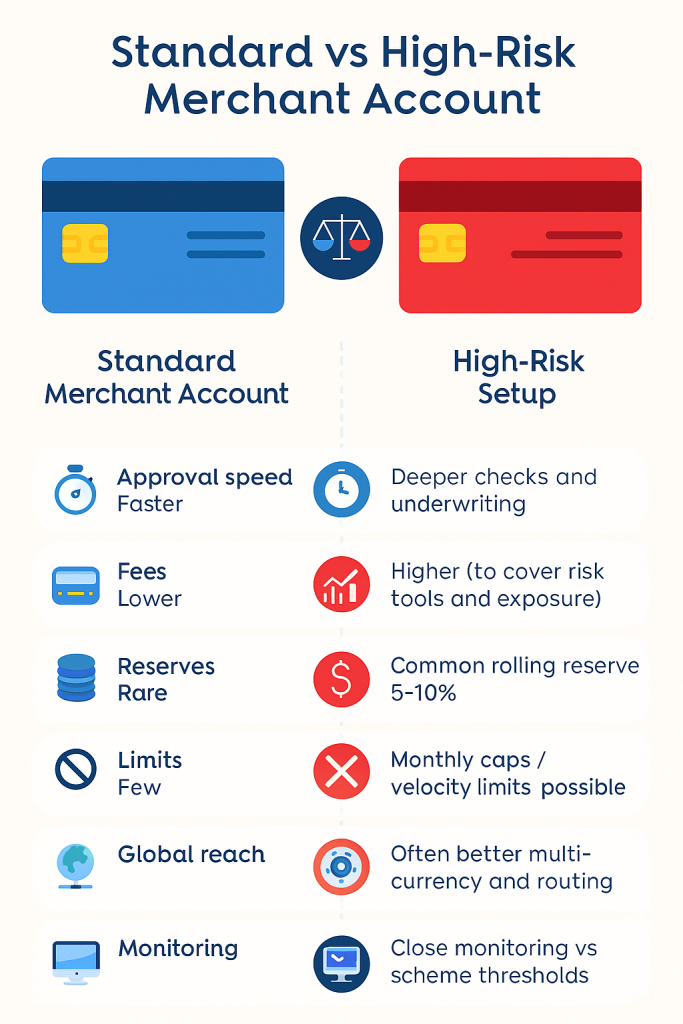

Unlike a standard merchant account, where businesses are trusted to handle payments with fewer issues, high risk merchant Accounts are designed with more protections for the bank or payment processor. This means stricter rules, but it also means traders can still run their business without facing constant account shutdowns.

Industries that often fall under the “high risk” label include:

- Forex and crypto trading

- Online gaming and gambling

- Travel and ticketing services

- Adult entertainment

- Health supplements and CBD products

- E-commerce stores selling high-value items

Traders in forex and crypto are commonly placed in this category because transactions are high in value, happen across borders, and often involve customers who may dispute payments.

To put it simply, High Risk Merchant Accounts are like a safety net for both banks and traders. Banks protect themselves from losses, while traders still get access to the payment systems they need.

In 2025, with financial markets becoming more digital, the use of these accounts is only going to rise. Traders need to understand that being labelled as “high risk” is not a bad thing; it is simply a sign that the payment industry is keeping an extra watch on industries where the risks are naturally higher.

Why do traders need high risk merchant Accounts?

Traders often find that a standard merchant account is not enough for how they work. Payments can be large, fast, and cross-border. When markets move quickly, customers may dispute charges, or banks may flag unusual activity. This is where High Risk Merchant Accounts make a real difference.

Problems with normal accounts-

- Chargebacks: Trading services can see more disputes when customers are unhappy with results or do not recognise a transaction. If the chargeback rate climbs, standard providers can issue warnings or even close the account.

- Cross-border payments: Traders accept clients from many countries. Different rules, currencies, and banks raise the risk of errors and disputes.

- Higher average ticket size: A small number of large transactions can look risky to banks, even when they are valid.

- Regulatory scrutiny: Sectors such as forex and CFDs face tighter rules. Banks want extra comfort that the business follows the rules and handles complaints fairly.

- Fraud attempts: Stolen cards, friendly fraud, and account takeovers are common in online finance, so providers need stronger checks.

What does a high-risk setup offer?

- Stability: You keep processing even if your sector is labelled risky. This helps avoid sudden freezes that can stop your business.

- Tools to control risk: Extra fraud filters, 3-D Secure, velocity checks, and better reporting.

- Multi-currency and global routing: Support for major cards, local methods, and settlement in different currencies.

- Clear limits and reserves: While not always fun, caps and rolling reserves reduce the provider’s exposure and keep the account open during busy or volatile periods.

Why this matters in 2025- Card networks watch dispute ratios closely. For example, Visa historically flags merchants with a 0.9% dispute ratio and 100 disputes in a month, with higher tiers for severe cases; Mastercard’s ECM/HECM tiers increase scrutiny above roughly 1.5% and 3% or high monthly counts. Staying under these levels keeps costs down and avoids fines.

How banks and payment providers assess risk

Providers look at the whole picture before approving or maintaining a merchant account. Here are the main factors they weigh.

1) Industry and business model

- Sectors such as forex, crypto-adjacent services, travel, tickets, and subscriptions are often marked as higher risk due to refunds, seasonality, and historical fraud levels.

2) Chargeback ratio and dispute history

- Your recent and long-term dispute rates per 100 transactions, monthly dispute counts, and how quickly you respond all affect risk scoring. Card schemes have monitoring thresholds (e.g., Visa around 0.9%/100; Mastercard tiered ECM/HECM) that providers must manage against.

3) Processing profile

- Average ticket size, spikes after promotions, weekend volumes, and cross-border authorisations. Sudden changes trigger reviews.

4) Geography and currencies

- More countries and currencies increase complexity. Sanctions, embargoes, and local rules also matter.

5) Compliance and operations

- Clear customer terms, risk warnings (where needed), refund policy, KYC/AML controls, and proof that marketing is fair and not misleading. In the UK and EU, CFD rules cap leverage and require risk disclosures, which providers check when assessing trading-related merchants.

6) Financial health

- Trading history, bank statements, and positive balances help. New firms may face tighter limits at first.

7) Reserves and settlement terms

- Many high-risk setups include rolling reserves to cover future disputes. Typical ranges are 5–15% of turnover for a defined period (for example, 90–180 days), with the earliest withheld funds released on a rolling basis.

Common Features of High Risk Merchant Accounts

Every trader who applies for a specialised account will notice some clear differences compared to a normal setup. These are not random, they exist to balance the risks for both the provider and the trader. Here are the most common features you will find in High Risk Merchant Accounts:

1) Higher transaction fees- Processing costs are usually higher because the provider invests in extra checks, fraud tools, and legal compliance. This may feel like a burden, but it is part of the price for having stable access to payment networks.

2) Rolling reserves- A percentage of your daily or monthly sales is held back for a set period. This safety net covers future chargebacks. For example, a 10% rolling reserve over 180 days means £1,000 of sales today has £100 held back until six months later.

3) Settlement delays- Standard accounts often settle within 1–2 business days. High risk setups may take longer (3–7 days), giving banks time to spot suspicious activity.

4) Monthly caps or limits- Some traders are given a monthly processing limit at first, such as £50,000. Once a good track record is proven, the limit can be raised.

5) Stricter compliance checks- Expect full Know Your Customer (KYC) and Anti-Money Laundering (AML) checks. Providers will ask for IDs, company documents, proof of address, and sometimes even marketing materials to confirm everything is in line with rules.

6) Multi-currency support- Because many high-risk businesses operate globally, these accounts usually support several currencies. This makes it easier for traders to serve clients in different regions.

7) Advanced fraud detection- These accounts often include built-in tools such as velocity filters (to stop too many transactions in a short time), geolocation checks, and 3-D Secure authentication.

8) Dedicated account managers- Many providers give traders direct support to handle disputes, monitor chargebacks, and keep the account in good standing.

Pros and Cons for Traders

Like any financial service, there are positives and negatives to consider. Understanding both sides helps traders plan better.

Advantages

1) Wider payment acceptance- Even if your industry is labelled “risky,” you can still accept card payments, digital wallets, and international transactions.

2) Business stability- The chance of sudden shutdowns is much lower. A high-risk provider expects volatility and disputes, so instead of closing your account, they apply reserves or tighter controls.

3) Global growth potential- Support for multiple currencies and cross-border routing means traders can expand without having to open many accounts in different regions.

4) Fraud prevention- Built-in fraud detection tools lower the chance of major losses. While no system is perfect, the protection is far stronger than what comes with a standard account.

5) Specialist support- Account managers often understand the trading sector. They can give advice on keeping disputes low, handling compliance, and negotiating better terms.

Disadvantages

1) Higher costs- Fees for processing, rolling reserves, and chargebacks are higher. For small or new traders, this can cut into profits.

2) Stricter approval process- Applying for High Risk Merchant Accounts takes more time and documents. Some providers may reject applications without a long trading history.

3) Limited flexibility at first- Monthly caps and long settlement delays can slow cash flow. Traders need to plan for this and keep enough reserves to cover expenses.

4) Reputation stigma- Being in the “high risk” category can feel negative. In truth, it is just a risk label from banks, but some partners may view it less favourably.

5) Funds on hold- Reserves mean some money is locked for months. This is safer for the provider but can be tough for traders relying on fast cash turnover.

The trade-off- For most traders, the benefits outweigh the downsides. While costs are higher, the ability to keep processing payments smoothly is critical. Without access to payment networks, the entire trading business could stop overnight. Accepting the terms of High Risk Merchant Accounts is often the only way to build long-term trust with banks and clients.

How to apply for a High Risk Merchant Account

Applying for High Risk Merchant Accounts is not the same as applying for a standard one. The process takes more time, requires more documents, and involves stricter checks. But if you prepare well, you can improve your chances of approval.

Step 1: Collect all business documents

Banks and payment providers want to see proof that your business is real and stable. Common documents include:

- Company registration certificate

- Tax identification numbers

- Bank statements from the last 3–6 months

- Proof of business address (utility bill, rental agreement)

- Identity documents for directors and owners

Step 2: Prepare financial history

A strong financial record helps build trust. Providers will want to know your turnover, refund rates, and average transaction size. If you are new, be ready to explain your business model clearly and show realistic projections.

Step 3: Be transparent about your industry

Do not try to hide that you are in a sector classed as high risk. If you trade in forex, crypto, or other flagged areas, state it upfront. Providers appreciate honesty and are more likely to help if they understand your exact needs.

Step 4: Show compliance measures

Traders who can prove they follow rules have a better chance of approval. Show your Know Your Customer (KYC) and Anti-Money Laundering (AML) policies, as well as clear refund and cancellation policies for clients.

Step 5: Choose the right provider

Not every bank or provider offers high risk solutions. Look for companies that specialise in High Risk Merchant Accounts. They will understand your industry and set terms that make sense for your type of trading.

Step 6: Expect a longer approval time

While a standard merchant account may be approved in a week, high risk applications can take several weeks. Be patient and use the time to prepare your systems for fraud monitoring and dispute handling.

Mistakes to avoid

- Hiding past chargebacks or disputes

- Applying with incomplete documents

- Using unclear marketing promises (like “guaranteed profits” in trading)

- Ignoring compliance questions

The role of technology and AI in 2025

Technology is reshaping the way payment providers handle risk. By 2025, artificial intelligence (AI) and advanced digital tools will play a major role in how high-risk merchant Accounts are managed.

- AI-powered fraud detection- AI systems now monitor transactions in real time. They learn from patterns and can flag unusual behaviour within seconds. For example, if a trader suddenly processes a series of large payments from a new country, the AI can hold those transactions for review before fraud occurs.

- Real-time risk scoring- Instead of waiting until the end of the month to check chargeback levels, providers use real-time dashboards. This allows both traders and providers to act quickly, adjusting filters or verifying customers before disputes happen.

- Blockchain and secure gateways- Blockchain-based payment gateways are becoming more popular. They offer faster settlements, transparent transaction records, and a lower risk of tampering. For traders dealing with crypto or digital assets, this adds another layer of trust.

- Biometric security- More providers are using fingerprint, facial recognition, or two-factor authentication to secure accounts. This makes it harder for fraudsters to break in or misuse accounts.

- Automated compliance- AI tools also help traders stay compliant with regulations. For instance, automated KYC checks can verify customer identities quickly, reducing manual work and lowering the risk of onboarding fraudulent clients.

Why does this matter for traders?

The future of High Risk Merchant Accounts is not just about higher fees and rolling reserves. It is also about smarter systems that allow traders to run safer, faster, and more reliable payment operations. Providers who invest in technology are better partners, as they help traders focus on growth instead of constantly worrying about fraud or chargebacks.

Payments are the foundation of every trading business. Without the ability to process money safely, even the best trading strategy cannot survive. This is why understanding and managing High Risk Merchant Accounts is so important in 2025.

We have looked at what these accounts are, why traders need them, how banks assess risk, and the features that make them different. We explored the pros and cons, the application process, and the impact of technology and global trends.

Yes, these accounts bring higher costs and stricter rules. But they also give traders stability, fraud protection, and the chance to expand globally. For many trading businesses, they are not just an option – they are the only realistic path forward.

The key lesson is that being “high risk” is not a negative label. It is a category that reflects the nature of online trading, cross-border payments, and fast-moving markets. With the right approach, traders can manage these accounts effectively and build long-term success.

Shikha Negi is a Content Writer at ztudium with expertise in writing and proofreading content. Having created more than 500 articles encompassing a diverse range of educational topics, from breaking news to in-depth analysis and long-form content, Shikha has a deep understanding of emerging trends in business, technology (including AI, blockchain, and the metaverse), and societal shifts, As the author at Sarvgyan News, Shikha has demonstrated expertise in crafting engaging and informative content tailored for various audiences, including students, educators, and professionals.