After a significant number of warnings from policymakers and analysts alike, rising equity valuations have been a growing source of concern, to the extent at which even the sell-side is becoming nervous about the outlook. Replete with the anxiety from analysts is the technical picture which increasing indicative of a potential momentum turning point after a spectacular multi-year bull run from the depths of the 2008-2009 financial crisis. Considering the risks ahead with the upcoming Bank of Japan and Federal Reserve monetary policy decisions, the pickup in volatility should be taken as a warning sign for potential investors as further tightening could precede a global asset reallocation. Although the S&P 500 remains not far from record highs, increased negative sentiment and downgraded views of the outlook will continue to stand in the way of further gains.

Complacency Abundant

Even though key Federal Reserve members have not deferred back to their language of “stretched” valuations and concerns about market “complacency”, the slew of sell-side downgrades makes the case for a steep correction more compelling. Goldman Sachs was the latest high profile sell-side institution to lower its S&P 500 forecast for year end, predicting 2100 as the level for the end of the year while the asset allocation team has turned bearish on the index. One of the main reasons behind this shift in sentiment is the growing possibility of the Federal Reserve raising rates once, if not twice, before the end of 2016. Higher interest rates might see investors more inclined to move towards other asset classes should yields improve, especially in fixed income. However, the two major factors that could say a lot about risk sentiment are the FOMC and BoJ.

The Bank of Japan has been notable in its influence in international financial markets, meaning any major disappointment in the coming week’s policy decision that sees the Yen strengthen could lead to a steep decline in risk assets. Besides the BoJ, heightened equity volatility generally accompanies FOMC decisions, meaning this week’s interest rate decision could be a game changer in terms of policy direction. Although the probability of action is low, with Fed Funds futures predicting a meager 12.00% chance of a hike, more hawkish guidance could change the calculus. Considering the faster pace of consumer inflation reported last week, with headline CPI printing at the highest level in 4-months, normalization could be coming sooner than anticipated, catalyzing a reversal in stocks. From a valuation perspective, the S&P 500 price-to-earnings multiple at 24.75 is significantly higher than the historical 15.61 average, meaning the benchmark remains historically overvalued and will eventually have to face the correction music.

Prices At A Turning Point

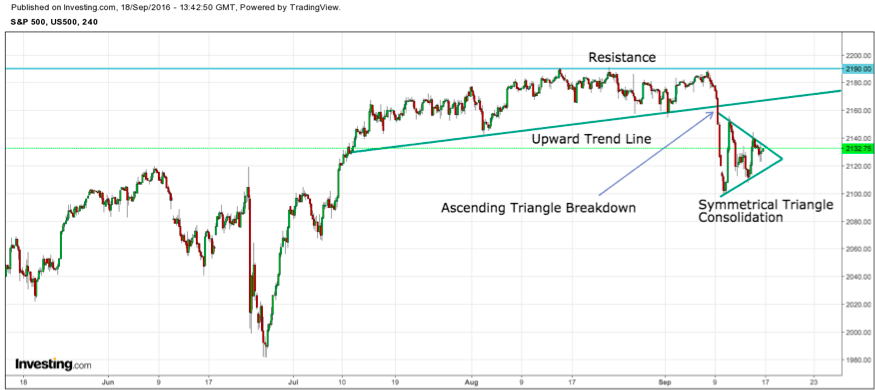

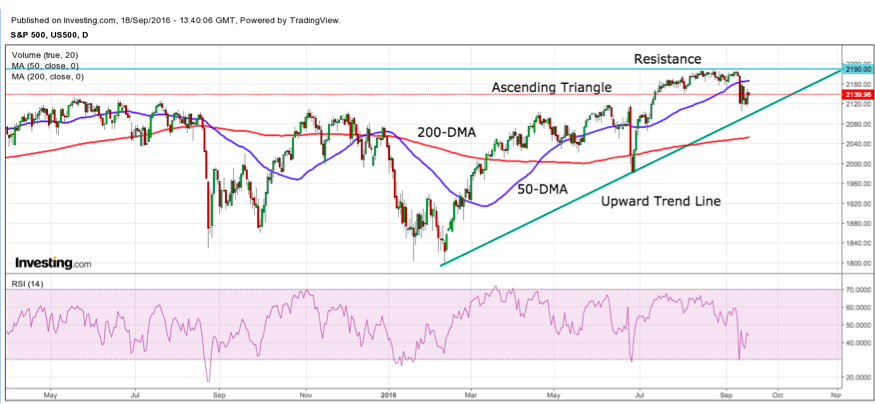

One of the key dynamics that has been in play for the last few months has been extremely low volatility and trading volumes, a normal characteristic of summer trading. As the old adage says, “sell in May and go away.” However, lower than average volumes and volatility that coincide with price consolidation are typically precursors to breakout momentum that results in either trend continuation or reversal. At this point, with very few drivers for upside in valuations from here, the downside correction is a more likely scenario. Bearing in mind the risk factors, should volumes and volatility continue to climb from here, it could be the early signs of a top in equity markets as upside momentum drivers disappear. After failing to complete an ascending triangle pattern and falling below the medium-term upward trend line, the S&P 500 has since been consolidating in symmetrical triangle.

Backing out the price action from a more medium-term chart, the price action of September 9th is clearly the biggest losing session in 43, marking the highest levels of volatility since the “Brexit” referendum. Looking at the longer-term upward trend extending from the March lows, it becomes clearer that the S&P 500 is setting up in another ascending triangle formation. However, after falling below the 50-day moving average, the simple moving average is acting as resistance against another upside rally whereas support lies at the trend line and the 200-day moving average which will soon converge on the trend line. Should this trend line and moving average be broken to the downside, it paves the way for a correction towards support at 1980 and beyond. One important item to remember about technical analysis is that any correction to a prevailing trend usually happens significantly faster than the move.

Looking Ahead

The S&P 500 is a tricky point in its valuation. Besides being vastly overvalued compared to more historical levels in terms of key metrics like the price-to-earnings ratio, key drivers of risk sentiment, namely sell-side recommendations, are being revised lower, indicating heightened potential of an oncoming correction. With a near-term consolidation in play and a longer-term consolidation underway, rising volatility and volumes could be a bad omen for valuations. Should the Bank of Japan hold off on new policy measures or the Federal Reserve take a more hawkish stance, the trigger for a deep reversal in the S&P 500 will be ever present. A reallocation of assets or onset of global risk aversion could accelerate any correction lower, suggesting that this week’s decisions come at a pivotal time for the directional momentum in the S&P 500.

Tradersdna is a leading digital and social media platform for traders and investors. Tradersdna offers premiere resources for trading and investing education, digital resources for personal finance, market analysis and free trading guides. More about TradersDNA Features: What Does It Take to Become an Aggressive Trader? | Everything You Need to Know About White Label Trading Software | Advantages of Automated Forex Trading