For the past few years, forex brokers have been crowing about the sheer size of the global forex market, with its $4 trillion daily trading volume dwarfing that of the stock market and other asset classes. Now, those figures look hopelessly out of date, after the release of recent data showing that there is now $5.3 trillion passing through the forex market on a daily basis.

The figures were released as part of the Bank of International Settlements (BIS) Triennial FX Survey in early September. This survey, which is made up of data aggregated from primary forex dealers worldwide during April 2013, countains a variety of information about how the forex market has changed and grown over time.

In what can be considered a milestone for both the retail FX industry and the BIS, retail data was included in the survey for the first time, including retail volumes and primary dealer volumes with retail driven counterparties. Intriguingly, the retail market volume was estimated at $185 billion, representing 3.5% of the $5.3 trillion figure for the market as a whole. The spot market accounted for the biggest share of this volume, with $78 billion, while FX swaps accounted for $74 billion.

Confusion reigns over true size of retail market

However, there is some disagreement over these figures, owing mainly to the fact that the BIS survey used ‘single counting’ for its calculations – which means that just one leg of the transaction is registered. With both legs taken into account, the volume of retail FX spot transactions is doubled to $156 billion per day. This brings it more into line with the figures quoted in Forex Magnates’ Quarterly Forex Industry Report, published in July 2013, which estimated the retail market as being worth $325 billion per day. At the time of the survey, it was assumed that this represented 8.1% of the $4 trillion per day forex market, but in light of the new figures, it would represent a more modest, but still substantial, 6.1% of the market.

Another possible reason for the large discrepancy between the two figures is that the BIS survey does not take into account retail volumes that are warehoused by market maker brokers, which represent at least half of the entire retail FX volume. Because the positions are not being processed on the open market, it would not be strictly accurate to say that they account for a percentage of the $5.3 trillion global forex market, and can be considered an entirely separate, albeit related, market.

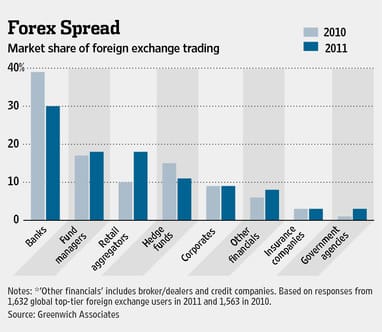

One thing that is undisputed is that the retail market is growing fast, with currency brokers that cater to retail investors almost doubling their share of trading volumes between 2011 and 2012, according to a survey by New York-based consultancy Greenwich Associates. This has coincided with a drop-off in forex activity among hedge funds between 2010 and 2012, falling from 15% to 11%, and banks, which fell from 39% to 30% due to an increase in the use of internal currency exchanges.

Meanwhile, forex brokers that offer retail trading (known as ‘retail aggregators’ saw their share grow from 10% to 18% over the same period, although retail trades only account for part of this figure. This places retail aggregators on a par with asset-management funds such as pension funds, which also saw their market share increase, albeit more modestly, from 17% to 18%.

The balance of power shifts

What this shift shows is that technology that was originally designed for use by fund managers, such as computer trading systems and high-speed network connections, is becoming more widely available to independent investors, democratizing and lending transparency to the FX market.

“The juggernaut that is retail FX is picking up steam,” said Peter D’Amario, a consultant who worked on the survey, adding that he expects retail aggregators to maintain this market share.

Retail aggregators, including companies such as Saxo Bank, OANDA, FXCM, and Gain Capital, select the best exchange rates currently available from the major banks and make them available to their clients, with a small margin added on in the form of the spread. This results in prices that are quite close to the wholesale interbank rates. As well as serving independent investors, these aggregators also serve small companies and even some funds.

The fall-off in the market share of banks is largely a product of new methods for exchanging money internally, rather than trading on the open market. This leads to greater efficiencies, minimising exposure to volatility. These banks have also been indirectly benefiting from the growth in the retail market by providing retail aggregators with rates.

A more recent release by Greenwich Associates, which despite lacking the depth of the 2012 survey, contains some interesting data, indicates that this trend continued into 2013:

“As a source of trading business, retail aggregators rank second only to banks, which generate about 26 per cent of global volume,” says Greenwich’s latest release.

Japan – and Mrs Watanabe – leads the way

Speaking to the Australian Financial Review, Dino Spinelli, head of foreign exchange sales for UBS in Australia and New Zealand, said: “Retail is becoming a force to be reckoned with. To some degree retail has taken market share from asset managers in 2013. People are looking at what retail is doing and why it’s doing it.

Source: Wikimedia Commons

“In Asia up to 40 per cent could come from retail traders in one day. In Australia retail is growing, but it’s not as big as in Japan, Singapore and Hong Kong. It’s part of the culture there.”

The retail forex industry has been growing fastest of all in Japan, due to what has been dubbed the “Mrs Watanabe effect” – the trend of housewives trading forex while their children are at school. Indeed, the huge amount of retail activity that occurs just after Japanese schoolchildren have been sent off to school has been known to cause bandwidth issues on some of Japan’s leading retail platforms.

“One example is what Japan retail did when the yen weakened,” said Spinelli. “They sold a lot of yen to buy US dollars. A lot of that positioning has been unwound. But they are a weight of money, so once they start in the morning, for example, we can estimate what will happen in the afternoon.”

Tradersdna is a leading digital and social media platform for traders and investors. Tradersdna offers premiere resources for trading and investing education, digital resources for personal finance, market analysis and free trading guides. More about TradersDNA Features: What Does It Take to Become an Aggressive Trader? | Everything You Need to Know About White Label Trading Software | Advantages of Automated Forex Trading