- Share prices reconnecting with fundamentals after spending the post IPO days buying the hype

- Management shakeup yet to prove any positive influence on results and company trajectory

- Rising revenues still offset by growing costs and weak monetization results from active users

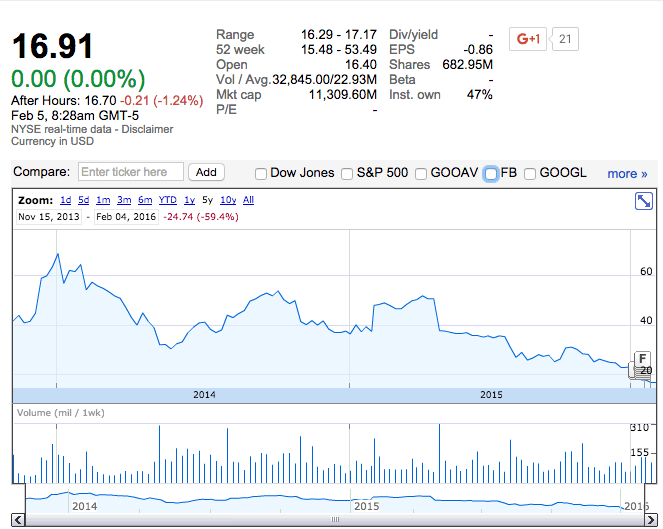

In spite of being one of Wall Street’s darlings for some time, the last year of performance from Twitter (TWTR:NYSE) has been abysmal, with obvious signs of growing revaluation pains for former high flying Silicon Valley beloveds across the market. Twitter in particular has been marred repeatedly for lacking a clear strategy, bad execution, and rather limited innovation outside of its flagship product. Vying for advertising dollars in the saturated social media space is especially challenging considering the competitive landscape. The one saving grace would be healthy growth in monthly active users, however, this is a longshot considering prevailing trends. Even though unsubstantiated takeover chatter earlier in the week sent shares higher temporarily, investors continue to take a beating ahead of the earnings announcement set for February 10th. With the odds still stacked against Twitter, it remains to be seen if management can somehow pull a rabbit out of the hat.

Source: Google Finance

A Company in Disarray

2015 was among the toughest yet for Twitter after a major shakeup on the executive level with Dick Costolo stepping away and Jack Dorsey filling the void. The reemergence of founder Jack Dorsey at the helm of Twitter has not done much to restore shareholder optimism as evidenced by the enduring carnage in the company’s valuation. More concerning than the founder being brought back to the helm after a disappointing stretch of execution failures is that Dorsey currently acts as CEO of another publicly listed company, payment technology provider Square (SQ:NYSE). At a time when both companies are unable to deliver profits and struggling to convey their vision to investors, Dorsey caught between two stools is a disaster waiting to happen.

With the pace of monthly active user growth gradually leveling off, Twitter will have to find a way to improve its user engagement times to harness more advertising revenues. Since crossing the 300 million user threshold, incremental user growth has experienced a tapering pace of expansion, adding to the growing possibility that the user base will actually shrink in coming quarters. Although the acquisition of Periscope was expected to help Twitter compete with the likes of Facebook when it came to video and continue growing its active users, so far the division has yet to show it can be competitive. More importantly however, is the fact that the company is unable to increase its engagement levels with users to increase their advertising value relative to peers.

Competition For Advertising Dollars Remains Fierce

As the mobile advertising market continues to show tremendous growth potential, the battle for eyeballs remains fierce and indefatigable. Twitter has continued to fall behind and many question the relevance of short messages as they do not command the same engagement like Facebook. In spite of the effectiveness of spreading messages through the platform and stronger monetization results from advertisers, users spend a fraction of the time on Twitter as compared to Facebook, with the latter outpacing the former by 10 to 1 in terms of minutes spent reviewing content. Aside from better engagement, Facebook generates nearly double the value per user from advertising, underlining the vast room for improvement for Twitter.

For the most part Wall Street firms are still touting price targets near $30.00 per share, telling clients to hold. However, unless Twitter can close the gap with other media and communications companies when it comes to generating advertising dollars, shares will remain depressed. Relative to other firms in the space and the broader market the underperformance has been significant. Based on current company activities and management shuffles, the sluggish pace of innovation and lack of a clear plan to address these issues means that turnaround aspirations are unlikely to be fulfilled over the medium-term. Absent shocking developments, finding a silver-lining in the financial results also proves elusive.

Fundamentally Speaking

Twitter shares are seeing little in the love department from financial markets, getting battered and bruised as the valuation gradually begins to reflect reality for a company struggling to define its relevance. Share prices have sunk over –77.00% since reaching post-IPO highs of $74.73, falling from grace and denting sentiment along the way. Even though revenues have experienced growth at a tremendous pace, net income remains firmly in negative territory as the company continues to drain cash from the balance sheet. Capital expenditures continue to rise while free cash flow sits in negative territory with the company yet to show income since inception. Although Twitter is on pace to exceed $3.00 billion in revenues for 2015, a valuation of $10.98 billion is rich unless the company can somehow control costs and show even marginal net income.

Strong margins mean nothing if cash flow is negative and all the gains are eaten away by costs. Value investors and income investors interested in long only portfolios would be wise to ignore Twitter, unless part of an elaborate M&A driven strategy. Though takeover chatter earlier in the week was quickly denied by Silver Lake Partners, it does not negate the fact that at the right valuation a buyer might be able to find value and monetize the Twitter platform to benefit shareholders. It remains a popular media distribution platform for spreading messages globally, but the monetization puzzle remains unsolved. In the meantime, forget about dividends and consider the short interest which currently sits at 9.96% of the total outstanding float. With abundant negativity, a near-term rebound in the valuation remains unlikely.

Conclusion

While revenue growth is finally starting to justify the valuation, Twitter remains a harbinger of times to come for other beloved listed technology companies that have yet to show shareholders any profits. After returning -57.07% in the last 52-weeks, Twitter is rapidly approaching its day of reckoning, likely to retest 52-week lows of $15.48 before sliding even further towards new record lows in the low teens. The combination of mismanagement, poor monetization results and a deficient strategy to spark a reversal in the company’s fortunes around means that Twitter could continue its slide until it becomes an attractive enough takeover target.

Tradersdna is a leading digital and social media platform for traders and investors. Tradersdna offers premiere resources for trading and investing education, digital resources for personal finance, market analysis and free trading guides. More about TradersDNA Features: What Does It Take to Become an Aggressive Trader? | Everything You Need to Know About White Label Trading Software | Advantages of Automated Forex Trading