Brexit negotiations remain in disarray following the announcement by the Speaker of the House of Commons that he will not allow Prime Minister Theresa May to put her withdrawal agreement to a third vote without substantial changes. British Parliament previously rejected the deal by a majority of 432 to 202 on 15 January, and again on 12 March by a vote of 391 to 242. Until Speaker John Bercow made his announcement, Prime Minister May was planning to put the matter to Parliament for a third time in advance of the EU summit on 21 March, with the intention of requesting a short-term ’technical extension’ if the deal passed. It is expected that she will look for alternatives but that she will have little choice but to request a long-term extension in order to craft a new deal.

In advance of the EU summit, we outline two Brexit scenarios and their expected impact on financial markets.

Scenario 1: Long extension (75%)

In the most likely scenario, the EU grants a long-term extension to Article 50. Prime Minister Theresa May stated last week that she will request a long-term extension if no deal has been approved by 20 March. According to political commentators, such an extension is likely to last years rather than months. It is uncertain, however, whether all EU member states would agree to such an extension, which would need to gain unanimous approval in the European Council.

EU negotiators have made it clear that they will not grant a long-term extension or further concessions if the UK isn’t intending to properly reassess its position on Brexit. Such an extension could open the door to alternative possibilities, like a very soft Brexit; a general election, possibly followed by a new government with a revised negotiating strategy; or even a second referendum with “Remain” as a possibility.

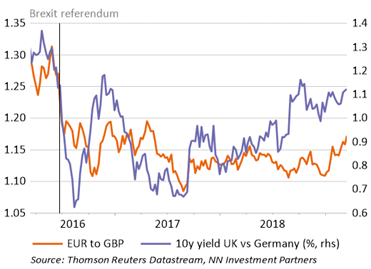

This scenario would have a positive impact on markets. Sterling and Gilt yields have already rallied significantly this year (see figure), as the market is pricing in a short-term extension. In the case of a longer-term extension, we project further rallies. We would expect Sterling to extend its 5% year-to-date gain against the euro and the 10-year Gilt yield to add to this year’s 9 bps rise versus its German counterpart in market anticipation of the Bank of England re-embarking on a monetary policy normalisation path. Of course, any normalisation would depend on UK and global economic conditions. We would also expect British equities to improve, in particular domestic sectors and real estate.

Scenario 2: No-deal Brexit (25%)

A no-deal Brexit is generally viewed as much less likely than a long extension, but it is also much more negative. In this scenario, the UK fails to agree on an extension with the EU and crashes out with no deal on 29 March. Although unlikely, this is possible. EU approval of an extension is by no means guaranteed, and approval would need to be unanimous. Some Eurosceptics have said they will lobby to get an EU member state to veto an extension as they seek to ensure a hard Brexit. Furthermore, several member states have made it clear that any extension should have a specific purpose. If the UK were to continue on its current negotiating path without revising its red lines, the EU would be unlikely to approve an extension. An extension would probably have to be approved at the EU summit on 21 March, so there would be little time to persuade any holdouts and the UK could end up crashing out by default.

This would have a very negative impact on markets, which have recently been anticipating a short-term extension. In particular, we would expect the Sterling exchange rate to depreciate versus all key currencies. Gilt yields would probably fall, as investors within UK markets would seek safety while the Bank of England would turn to further easing measures to cushion a short-term growth shock. We would expect British domestic equity sectors and real estate to be hit particularly hard. To a lesser extent, this would also be a negative event for risky assets globally, especially in Europe.

EU will probably grant extension, but no-deal Brexit is still on the table

It is believed that the EU would probably grant an extension to Article 50 if the UK requests one. Germany and other large EU member states have expressed an overt willingness to be flexible, and these countries could exert pressure on smaller countries. Donald Tusk, President of the European Council, has also asked the EU to be open to an extension. Moreover, a no-deal exit on 29 March would be in no one’s best interest, so it is expected that the UK and EU will reach some kind of extension agreement and thus avert catastrophe. Still, the often turbulent Brexit process has made it clear that no option, however perilous, is off the table.

Tradersdna is a leading digital and social media platform for traders and investors. Tradersdna offers premiere resources for trading and investing education, digital resources for personal finance, market analysis and free trading guides. More about TradersDNA Features: What Does It Take to Become an Aggressive Trader? | Everything You Need to Know About White Label Trading Software | Advantages of Automated Forex Trading

{kind=link}